Trending

Your First $10M Tax-Free!

Section 1202 Stock: What Founders and Employees Need to Know About The QSBS Gain Exclusion

A little-known tax incentive intended to spur investment in small businesses can help startup founders, early employees and investors retain millions of dollars in their personal wealth. The incentive, known as qualified small business stock (QSBS) lets people who own shares early enough in a company’s life avoid tax on some or all of the proceeds.

We recently spoke with Ray Thornson, a Managing Director at Andersen Tax, about what people with startup shares should know about QSBS. He explained the rules and regulations, and what people can do today in order to lock in savings later.

What is Qualified Small Business Stock?

Qualified small business stock is a provision in the tax code (U.S. Code Section 1202) that provides some tax benefits for individuals that invest in early-stage companies. The provision has been in our tax code since 1993. It’s only become well known in the last year or so because, historically, it didn’t provide a material tax benefit. But that changed when the federal capital gains rate increased in 2013 and the percentage exclusion for QSBS increased from the original 50% for stock that would qualify for QSBS treatment around that time. Taken together, these changes make for a useful but underutilized benefit that investors in small businesses can use to their advantage.

So, what are the benefits now?

There are two main benefits to Section 1202: the exclusion and the rollover provision (the rollover provision will not be discussed at length here). If, upon acquisition of the stock, the company is considered to be a qualified small business and you hold the stock for at least five years, then upon the sale of that stock you could exclude from taxation a portion or all of the gain, depending on how much you have. So that’s the key. If you hold the stock for at least five years, after the date of taking ownership, you can exclude a meaningful portion of the gains. For employees, “acquisition of the stock” typically means being granted restricted stock or exercising their ISO/NSO stock options. For investors, that’s a function of purchasing stock in the company.

This is also where it gets a little complicated: prior to February 18, 2009, the exclusion percentage was 50%, meaning you were allowed to exclude half of the eligible amount of gain. Between February 18, 2009 and September 27, 2010, that went up to 75%. As of September 28, 2010, it’s 100% of the gain up to $10 million or 10 times the base investment, whichever is greater. So if you’re an investor who put $3 million into a business with QSBS, you could actually exclude up to $30 million.

It sounds great on paper, but is this something that real people at actual startups can benefit from?

People are saving significant amounts of tax dollars from this and keeping that money within their estate for future wealth building.

This is a relatively new topic for a lot of people out there because, at the federal level, the material tax benefits have not been significant, so no one’s really paid attention to it; but changes in recent years have made qualified small business stocks a more viable option.

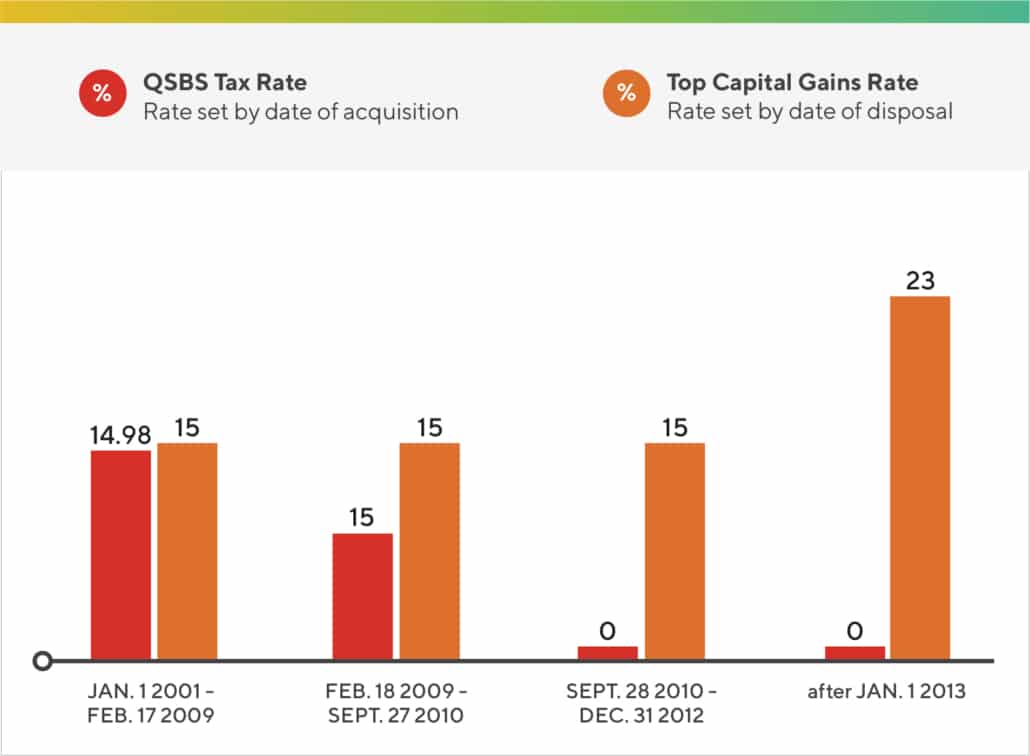

Tax code changes have made the benefits of QSBS more pronounced:

*Includes 3.8% Obamacare surcharge

Prior to 2013, the capital gain rate was 15%, so if you sold your company and you made $10 million and you didn’t have QSBS, at the federal level you would pay $1.5 million of tax. Instead, if you qualified for QSBS, then you got to exclude $5 million and on the $5 million you didn’t exclude, the tax rate was 28%. It’s kind of quirky, but it’s just in the rules.

So on the gross gain of $10 million, the effective rate is 14%, right? In addition to that, 7% of what you excluded or $350,000 counts as income for alternative minimum tax (AMT) purposes. That equates to 98 basis points on the additional tax rate, so now you’re at 14.98%.

So, as I said, if you don’t have QSBS, you pay 15%. If you’ve got QSBS, your tax rate was 14.98%, so on a $10 million gain, your exact savings were $2,000. It just wasn’t anything to really get excited over regardless of whether people were aware of it or not.

Now, what has happened is the 15% rate that you’re comparing the QSBS rate to has gone up to 23.8% because capital gain rate went from 15% to 20%, and the Affordable Care Act Medicare Tax of 3.8% on investment income was added. The savings are more material.

The other part is the exclusion has gone up to 75% or 100%. In the case of 100%, there’s no complicated math. It’s just a lot of extra money in someone’s pocket.

What is QSBS and how does a business qualify?

The most well-known qualification is that at the time an individual receives stock in the company—whether it’s a founder who gets founder stock, an employee who exercises stock options, or an investor who purchases preferred stock—the assets on the company’s balance sheet need to be under $50 million.

For a lot of companies, you can measure the $50 million asset threshold by looking at how much money the company has raised. If they’ve raised under $50 million in total, then there’s a good chance that they’re going to meet this requirement.

Intellectual property counts as an asset, too. If the intellectual property was developed by the company, then the value of that intellectual property would likely be the amount of money that they spent to develop it and capitalize it on their books. If, instead, the intellectual property was contributed to the company in exchange for stock, then for purposes of the $50 million asset threshold, you will use the value of the intellectual property upon contribution.

Are there other qualifications?

The business has to be a C corporation. It can’t be an S corporation and it can’t be an LLC.

However, if you start out as an LLC then convert to a C corporation, then you could start to qualify on the date of conversion. It also has to be domestic. You can’t be incorporated in the Cayman Islands or overseas.

The last big issue for qualification is whether the business itself qualifies. The easiest way to think about that is by looking at what is not a qualified business, which tends to be the types of businesses that are highly service-oriented.

This was done for a couple of reasons. First, to incentivize investors to put their money in small businesses. Secondly, it was really to focus on businesses that — while it’s unclear if we thought in such terms in 1993 — were scalable. So the types of businesses that don’t qualify: hotels, motels, restaurants, accounting firms, law firms. Those are all service-oriented.

The vast majority of the companies that are formed in the Bay Area will qualify because they tend to revolve around technology and the creation of technology, software, and hardware. And these companies that are very scalable.

If I acquired my options before my startup had $50 million in assets and by the time the five-year holding period is over we’ve taken on $100 million in cash and lost the qualified small business status, do I still get to claim QSBS for the stock?

Two things on that. Number one: the key is the asset amount at the time you acquired your stock. It doesn’t matter if the next month your company raises a bunch of money as long as when you acquired the stock, you met the asset threshold of being under $50 million. The other thing to consider is that, let’s say the company is over $50 million of assets. If it’s over $50 million of assets, any stock issued after that will not qualify even if it subsequently goes under the $50 million asset threshold. Once it goes over, then no future issuances of stock can qualify and no future exercises of options can qualify.

Another hypothetical: Say my startup has $30 million in assets. I get my option. By the time I exercise my option, we have $51 million in assets. Does that still qualify as QSBS?

No, it’s all measured at the time that you exercise your stock. If you exercised your stock and you’re already over $50 million, then you don’t get QSBS. It doesn’t matter when it’s granted.

The way to think about this is, if you’re an early employee at a startup, there has historically always been an incentive to exercise early. If you’re bullish on the company and you think its value is going to go up, if you exercise early, that starts the holding-period requirement to get capital gains. QSBS provides even more incentive to do so, to exercise as early as possible before the company gets too big.

Have companies accepted smaller investment rounds or turned down money to stay under the threshold?

They’re starting to be more aware of this issue. Let’s say there’s $40 million on a company’s balance sheet, and they’re raising $20 million. If you’re investing in that round that puts you over $50 million, then the stock you get in that round does not qualify. So maybe you would plan on approaching the round a little differently, so that the investors who care about QSBS are positioned to take advantage of it.

What would I need to do in order to actually get that treatment?

One thing I encourage everyone to do is to keep a file, whether virtual or otherwise, of all the information they need to support the position that it’s QSBS. You’d like to document the $50 million asset threshold. That’s easy for the founder because you just put in your file a copy of the balance sheet from the tax return for the year in which you acquired the stock.

The other stuff is pretty straightforward: the domestic C corporation designation, for example. You could just have the company represent that in a letter.

It could be several years down the road when you actually exclude the gain on your return, and let’s just say another two years after you filed your tax return that you may get audited. If you didn’t ask for this information way back then, you could have nothing to do with that company in the future. It’s now this big company that’s very private about its information, it could be hard to get what you need.

Otherwise, the first time this has to be disclosed is the year in which you think you’ve held the stock long enough and you exclude that gain on your tax return.

What takeaways or parting advice would you offer?

If an employee has conviction in their company, exercising vested shares as early as possible, and in a consistent manner as additional shares vest, will ensure that they maximize their QSBS benefit. Albeit cliche, to make sure you’re doing this right, it is prudent to make sure your tax adviser has a good handle on the QSBS rules and opportunities that may be afforded to you under these provisions.

Related Blog Posts

https://www.founderscircle.com/wp-content/uploads/2023/11/State-of-Venture-Debt-Blog-Banner-800x400-1.png

400

800

hannah@fcc.vc

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

hannah@fcc.vc2023-11-17 17:37:552024-05-24 01:39:29The State of Venture Debt

https://www.founderscircle.com/wp-content/uploads/2023/11/State-of-Venture-Debt-Blog-Banner-800x400-1.png

400

800

hannah@fcc.vc

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

hannah@fcc.vc2023-11-17 17:37:552024-05-24 01:39:29The State of Venture Debt https://www.founderscircle.com/wp-content/uploads/2019/09/10ThingsToKnow409A_Thumb.jpg

1390

1390

Avalaunch Media

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Avalaunch Media2022-01-25 10:55:362024-05-22 20:23:28The 409a Valuation Process

https://www.founderscircle.com/wp-content/uploads/2019/09/10ThingsToKnow409A_Thumb.jpg

1390

1390

Avalaunch Media

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Avalaunch Media2022-01-25 10:55:362024-05-22 20:23:28The 409a Valuation Process https://www.founderscircle.com/wp-content/uploads/2019/09/SmarterEquity_Thumb.jpg

1389

1390

Wonderly Care

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Wonderly Care2022-01-23 17:12:262024-05-23 23:52:38Stock Options and Other Equity Compensation Strategies

https://www.founderscircle.com/wp-content/uploads/2019/09/SmarterEquity_Thumb.jpg

1389

1390

Wonderly Care

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Wonderly Care2022-01-23 17:12:262024-05-23 23:52:38Stock Options and Other Equity Compensation Strategies