Trending

M&A Considerations During a Pandemic – Qatalyst Fireside Chat

The CEO|Circle came together with James Kim + Nadir Shaikh of Qatalyst Partners to discuss M&A considerations during COVID19. During these challenging times, Qatalyst shared how CEOs can and should cultivate meaningful relationships on both sides of the M&A equation.

The Key Takeaways:

Current Market Conditions: Post-Covid Valuations are Difficult. The last two years were as strong as we’ve seen since the late ‘90s in the M&A and IPO markets, but Covid has turned the markets upside down. Valuation and competing priorities are now headwinds for getting deals across the line. For buyers, the lack of visibility into valuation, the importance of protecting cash, and the prioritization of keeping the core business in order makes this a difficult time to be proactive about a process. For sellers, this is not a great time to have the most competitive process. For both parties, just the inability to meet face-to-face all but precludes transactions from taking place.

It’s Time to Network. This is an excellent time to start dialogue and cultivate relationships with strategic partners. Whichever side you are approaching the conversation from (buyer, seller, partner), there is no rush to turn the conversation into action in this environment. When markets normalize and transactions pick up, you will be better positioned to act accordingly if you proactively build those relationships now.

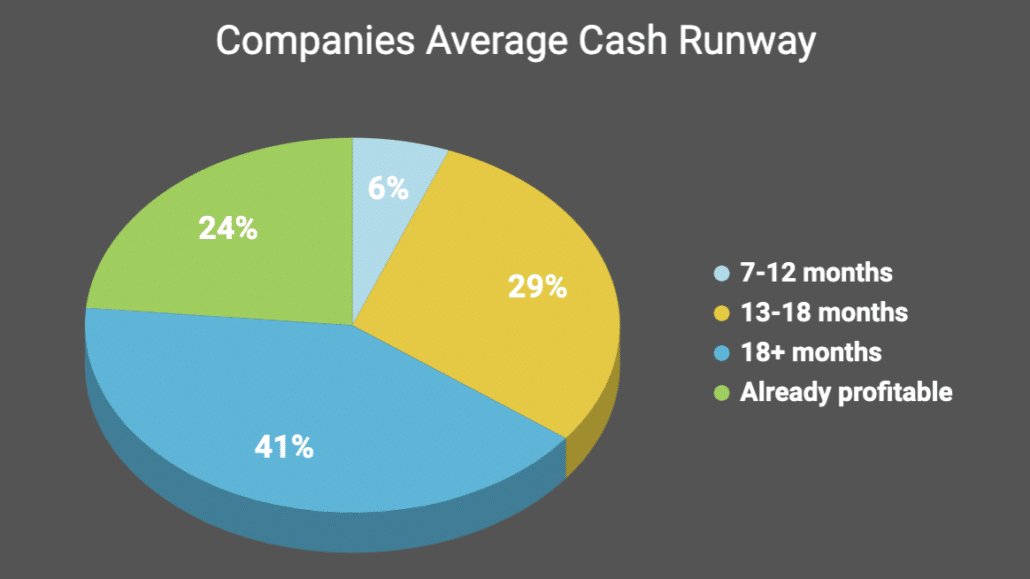

Cash is Still King. All companies are optimizing for cash through both cost-cutting and borrowing. There is plenty of access to debt financing out there, especially for the most creditworthy borrowers – although the terms may not be as favorable as they were 3-6 months ago. Large public companies are strengthening their balance sheets, and while there is some speculation that some of this is to bolster reserves for acquisitions, the primary objective is simply to preserve cash. (More on cash preservation in the takeaways from the CFO|Circle call on Financial Planning.)

Approaching Various Transactions in the Current Environment:

- Strategic Financing & Partnerships. Strategic buyers are increasingly interested in participating in equity financing. It is a way to slow-play getting close with potential strategic targets in an unattractive M&A environment. Companies are also very open to high value-add strategic partnerships, and you can likely enter into partnerships on more favorable terms than pre-Covid.

- Things to Consider: Not all capital is created equal. You need to really weigh the deal terms when taking on strategic equity financing – be sure that the terms do not prevent a competitive M&A process in the future, and be sure that you aren’t creating optics that will prevent other strategics from wanting to get involved later on. Be aware that just because a strategic invests in a company doesn’t mean it will ultimately proceed towards M&A.

- Tuck-In Acquisitions. Very early-stage companies with promising products/technology may have a hard time raising the next round of financing. This may create opportunities to make highly strategic tuck-in acquisitions.

- Things to Consider: Cash is Still King. Using equity to make acquisitions can help you optimize for cash.

- Merger of Equals. A merger of equals that results in strong synergies through scale or cost savings can be a proactive strategy to survive the crisis and come out stronger on the other side.

- Things to Consider: Working through governance and social issues in a true merger of equals can be complicated. Who is in charge? What is the board compensation? What are the reporting lines? If you exhibit openness up front to being less contentious on these points you may be able to accelerate the process.

Related Blog Posts

https://www.founderscircle.com/wp-content/uploads/2024/03/03.13-Scaling-Yourself-Redefining-Growth.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-19 14:35:162024-03-25 07:37:36Advancing Your Influence: Strategies for CFOs

https://www.founderscircle.com/wp-content/uploads/2024/03/03.13-Scaling-Yourself-Redefining-Growth.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-19 14:35:162024-03-25 07:37:36Advancing Your Influence: Strategies for CFOs https://www.founderscircle.com/wp-content/uploads/2024/03/03.15-Scaling-Yourself-Redefining-Growth-1-copy.jpg

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-18 15:25:122024-03-25 07:37:44How People Leaders Can Invest In Their Own Growth

https://www.founderscircle.com/wp-content/uploads/2024/03/03.15-Scaling-Yourself-Redefining-Growth-1-copy.jpg

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-18 15:25:122024-03-25 07:37:44How People Leaders Can Invest In Their Own Growth https://www.founderscircle.com/wp-content/uploads/2024/02/Bold-Leadership-CHRO-Header.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-02-23 01:00:312024-03-25 07:37:525 Levers of Leadership: How CHROs Can Foster a Resilient and Efficient Workforce

https://www.founderscircle.com/wp-content/uploads/2024/02/Bold-Leadership-CHRO-Header.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-02-23 01:00:312024-03-25 07:37:525 Levers of Leadership: How CHROs Can Foster a Resilient and Efficient Workforce