Trending

Scenario Planning in the Age of a Pandemic

CFO’s, today’s “Risk Officers”, convened with Rob Krolik (who leads the CFO|Circle Masterclass series) to discuss how to scenario plan around a financial downturn (COVID-19), including how to model cash preservation and assumptions to make around revenue and expenses.

First, know that there’s a light at the end of the tunnel, even if we aren’t facing a V-shaped recovery. But what you do today will be much more important than what you do at the end of the pandemic with the goal being to make sure your company survives. Also, keep your board updated on a weekly or biweekly basis, as this will instill confidence that your team is on top of the problems arising from the pandemic.

Recommendations for financial planning in the age of COVID-19 include:

Cash is King: Companies are advised to ensure they have at least 18 months’ runway and to closely monitor their cash position. Creating a weekly or even daily cash report for all of your company’s cash accounts is a good way to keep a pulse on your cash position. Furthermore, with an eye towards optimizing for cash preservation versus a vehicle to earn interest, this isn’t the time to be holding cash in bonds or munis. Utilize money market funds for cash preservation (forget the interest). Take a look at what your company is invested in and reallocate as necessary.

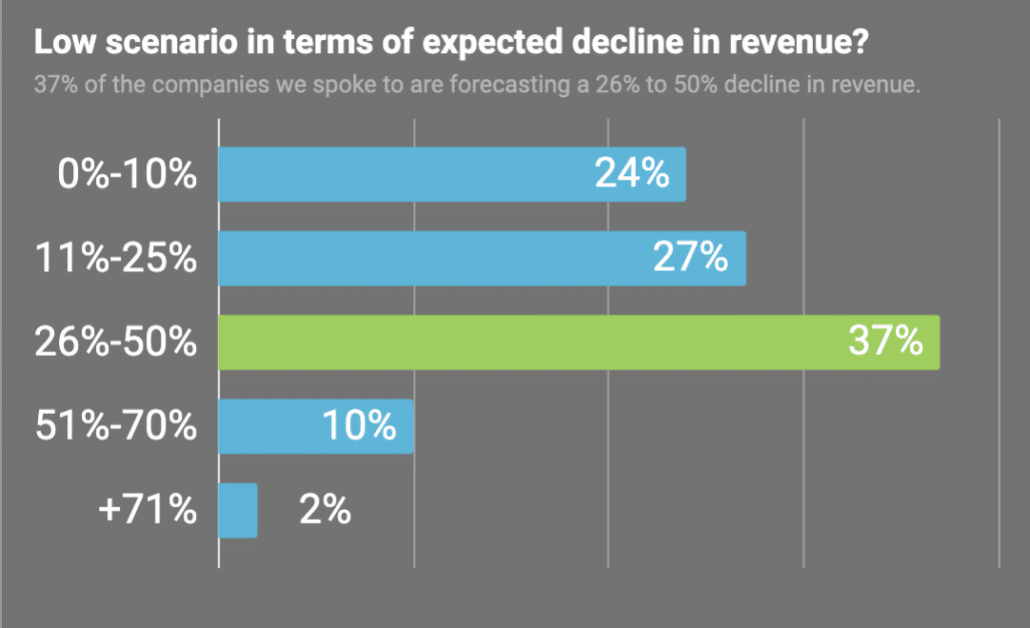

Projecting Forward: Run three revenue scenarios: (1) original 2020 plan, (2) 10% decline in revenue 2019 to 2020, and (3) 50% decline in revenue 2019 to 2020. Take a look at your company’s data from the last two to three weeks and see where along the spectrum of scenarios your company would align most closely to if you project forward what this trending data means (which might help to dial-in the % decline in revenue you should be modeling) and assume no funding events are available this year.

Cutting Burn: After calculating your cash balance and therefore determining your monthly burn rate target for having 18 month’s cash, you’ll need to figure out how to cut burn. Start out by cutting marketing spend by 50% or more, since marketing is unlikely to break through pandemic news at the moment. Then, determine the number of FTEs that will need to be let go in order to reach your burn and allocate those cuts across teams to match your corporate priorities over the next 18 months. Don’t do a peanut butter approach, be strategic.

Accounts Receivable: As companies seek ways to preserve cash, delays in paying AR are surfacing. Assuming the 80/20 rule, where 80% of your revenue could be coming from 20% of your customers, you should focus on the sectors those 20% of customers are in and note that collectability is likely to be down (possibly to 50%) for customers in the free citation generator hospitality industry, for example. Furthermore, you’re more likely to be paid if you reach out to your customers, so frequently and consistently request payments, be the squeaky wheel. If need be, consider offering a 10% discount to customers who pay right now.

Leading Indicators for Measuring your Business: AR collections, SDR top-of-the-funnel analysis (how many meetings are getting scheduled, pushed, or cancelled), pipeline aging, and conversions. Also helpful to break down all of this analysis by customer vertical.

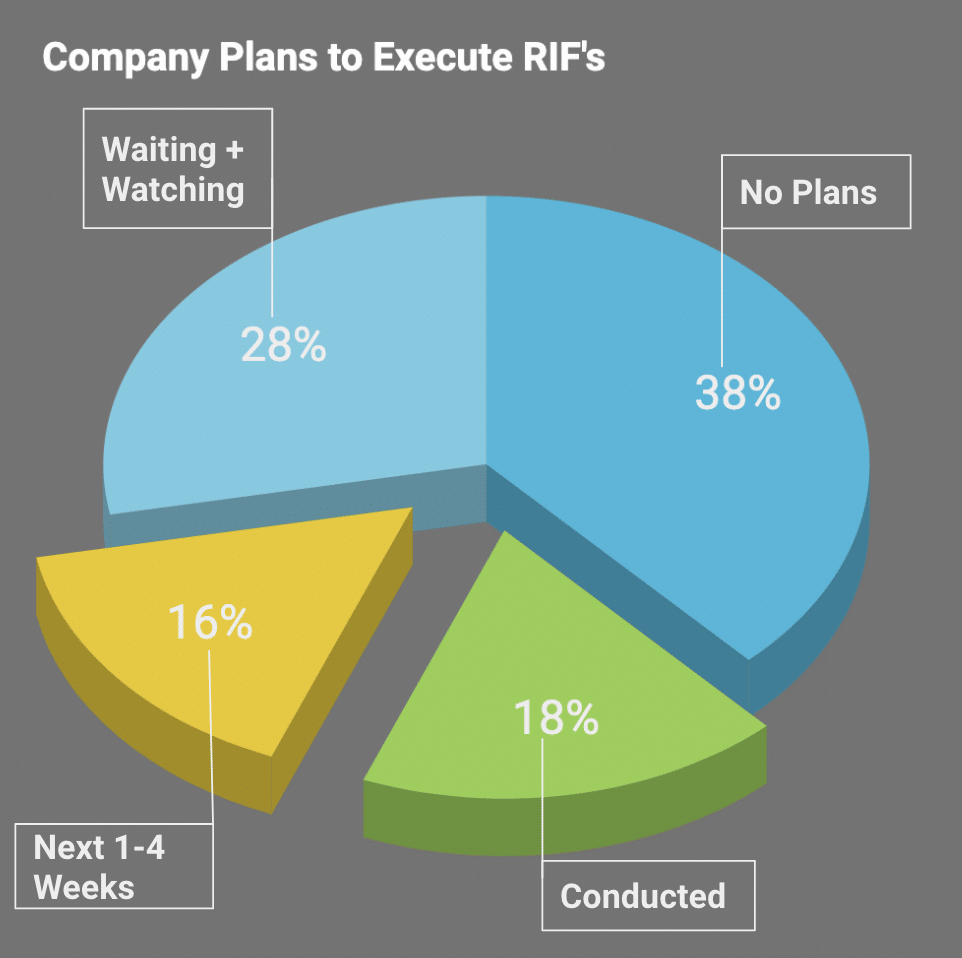

RIFs: Whether or not your company has 18+ months’ runway, a RIF might be a discussion topic amongst your leadership team and your board since 70-80% of costs tend to be people. It’s important for RIFs to be one-and-done, so you can move forward and also not risk further hits to your team’s morale.  Meanwhile, RIFs might be on the table for companies with sufficient runway – if your board is suggesting this, force them to be transparent around the reasoning for a RIF so that you can conversely be transparent with your team. Discuss RIFs with managers in terms of the number of people, not dollar amounts, and plan for the worst case scenarios when determining the number to cut. If you hand out targets in dollar amounts, managers will find creative ways to hit their numbers creating circular conversations and drawing out the process. Know that it’s likely that managers will come back and say “I can only cut 13, not 15” and that’s fine.

Meanwhile, RIFs might be on the table for companies with sufficient runway – if your board is suggesting this, force them to be transparent around the reasoning for a RIF so that you can conversely be transparent with your team. Discuss RIFs with managers in terms of the number of people, not dollar amounts, and plan for the worst case scenarios when determining the number to cut. If you hand out targets in dollar amounts, managers will find creative ways to hit their numbers creating circular conversations and drawing out the process. Know that it’s likely that managers will come back and say “I can only cut 13, not 15” and that’s fine.

Related Blog Posts

https://www.founderscircle.com/wp-content/uploads/2024/03/03.13-Scaling-Yourself-Redefining-Growth.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-19 14:35:162024-03-25 07:37:36Advancing Your Influence: Strategies for CFOs

https://www.founderscircle.com/wp-content/uploads/2024/03/03.13-Scaling-Yourself-Redefining-Growth.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-19 14:35:162024-03-25 07:37:36Advancing Your Influence: Strategies for CFOs https://www.founderscircle.com/wp-content/uploads/2024/03/03.15-Scaling-Yourself-Redefining-Growth-1-copy.jpg

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-18 15:25:122024-03-25 07:37:44How People Leaders Can Invest In Their Own Growth

https://www.founderscircle.com/wp-content/uploads/2024/03/03.15-Scaling-Yourself-Redefining-Growth-1-copy.jpg

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-03-18 15:25:122024-03-25 07:37:44How People Leaders Can Invest In Their Own Growth https://www.founderscircle.com/wp-content/uploads/2024/02/Bold-Leadership-CHRO-Header.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-02-23 01:00:312024-03-25 07:37:525 Levers of Leadership: How CHROs Can Foster a Resilient and Efficient Workforce

https://www.founderscircle.com/wp-content/uploads/2024/02/Bold-Leadership-CHRO-Header.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-02-23 01:00:312024-03-25 07:37:525 Levers of Leadership: How CHROs Can Foster a Resilient and Efficient Workforce