Trending

Running an Employee Tender Offer Without a Big Tax Hit: How to Structure a Secondary So it Doesn’t Count as Compensation

As employee tender offers increase in frequency, so too has the scrutiny applied by auditors. Among the questions asked during these reviews: Is a buyback a straightforward sale of stock, or is it in part a form of compensation for employees?

The answer can have big implications for the transactions, both in terms of how much money participants get to take home, and what, if any, extra costs companies need to pay. As with many issues in the evolving secondary-transaction field, the answer isn’t black and white.

We recently spoke with Cindy Hess, Mark Leahy, and Shawn Lampron, all partners at Fenwick & West, about the laws and regulations concerning compensation, how they’re applied to employee tender offers, and what steps companies can take to maximize the benefits to employees, and reduce cost and future risk.

We recently spoke with Cindy Hess, Mark Leahy, and Shawn Lampron, all partners at Fenwick & West, about the laws and regulations concerning compensation, how they’re applied to employee tender offers, and what steps companies can take to maximize the benefits to employees, and reduce cost and future risk.

How does the issue of compensation come into play in employee tender offers?

In the last five years, secondary sales have become an expectation in Silicon Valley. With that comes the additional hurdle of an organization’s tender offer tax treatment. The question of whether some of the proceeds from a sale should be considered compensation comes into play when these transactions are done above the current option price or the 409A value.

In the last five years, secondary sales have become an expectation in Silicon Valley. With that comes the additional hurdle of an organization’s tender offer tax treatment. The question of whether some of the proceeds from a sale should be considered compensation comes into play when these transactions are done above the current option price or the 409A value.

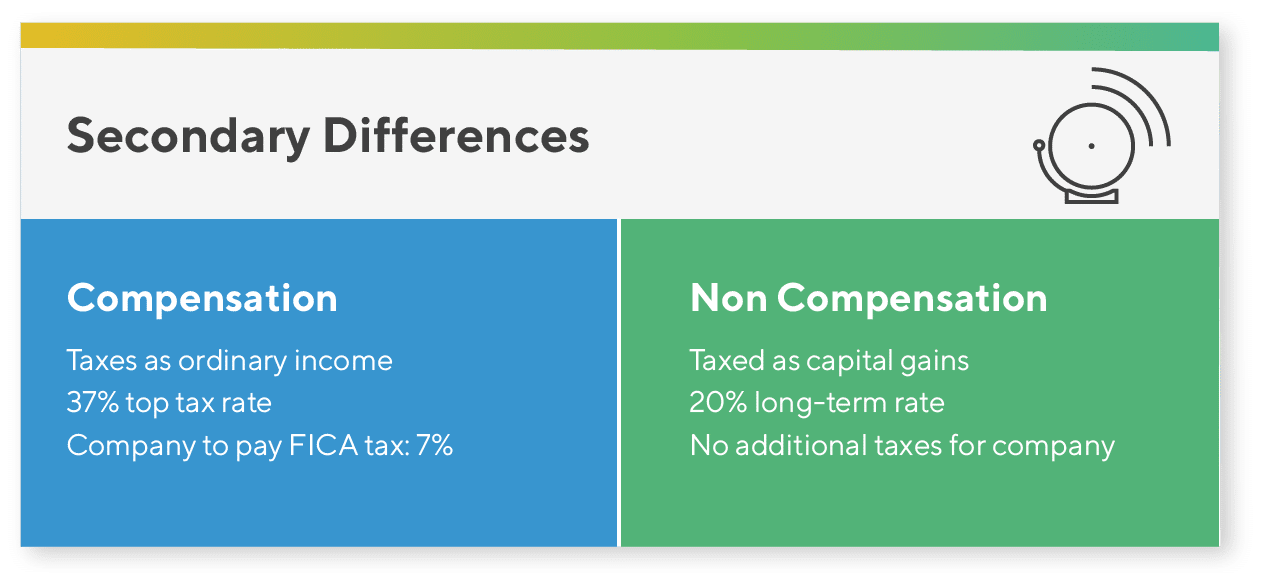

Compensation income is subject to ordinary income tax rates. Currently, the highest rate is 37%. In addition, employers pay FICA tax, which includes Social Security and Medicare, and which can be another 7.645%. Long-term capital gains, where you’ve held stock for at least a year, are taxed at a maximum of 20% and are not subject to FICA. So that can make a big difference.

These days, that premium over the 409A valuation in a tender offer is often greater than in the past, so there’s more attention to this issue. Accountants have also been more conservative on this point in recent years.

It seems like it should be straightforward. You buy shares at one price, and then you sell them, hopefully, at the highest price you possibly can get, and the difference is capital gains. Why is this any different?

Because these are essentially insider transactions. The issue for the company and the board is that they need to grant options to employees and those have to be priced at fair market value, or there are penalties for the employer and the employee.

You can’t say, “Well, I think the true fair market value of common stock for purposes of issuing options is $2, but the true fair market value of common stock for buying back stock is $6.”

It’s different if you have an outsider who comes in and says, “I don’t know much about this company, but I have a lot of faith in it so I’m going to pay X dollars,” and that turns out to be more than the 409A value. You can look at that and say people have different views of value.

Then there’s a big middle ground where the buyer has some sort of relationship with the company.

What are the factors that might determine whether it’s an inside transaction?

A big one is: how much information does the buyer have, and how informed is the judgment on value? Another is motivation. Is someone trying to convey value to employees?

If the motivation is to convey value to employees—and this is a legal term that will often trump the fact that most shareholders have their own profit motive—then employees should be taxed on that premium. If your employer gives you a brand new car, you’re going to be taxed on that. If it wasn’t taxable, every CEO in the United States would be paid in the form of cars. Similarly, if someone gives you cash in excess of the value of a car that they’re buying from you, that’s compensation. In some cases, that’s what’s going on with these stock sales.

At the same time, companies are seeing that there are people who are willing to pay more than the 409A value—people who are willing to pay for the expectancy-value as opposed to value today. Whereas the 409A value is intentionally a cautious valuation that reflects the fact that oftentimes companies don’t have exit events.

Is this a black-and-white issue?

Some will argue that you can buy back at a price above the 409A, and they make different arguments, including that there’s not really a market at that higher price. Our view is that’s a hard argument to win with the IRS where the company or an insider is paying a premium.

The nuance is that there’s language in the tax regulations that says if a stockholder gives compensation to an employee, then that’s treated as if it were payment from the company. So then the question is: In what circumstances is the stockholder paying compensation to employees? That’s where it’s a gray area.

Here are two real examples. We had one buyback arranged by a party that already owned 50% of a company. The consensus view is that’s the same as the company, so any premium is compensatory.

We had another case where it was an 18% stockholder. Our view is that it’s not compensatory, because it doesn’t make sense for that stockholder to carry the entire burden of compensation on their backs to the benefit of all stockholders.

Oftentimes, there are other factors you can point to. In this instance, the stockholder has investing guidelines that says that it has to have at least X%. It bought in the preferred round but it really wanted a lot more stock, and it would have bought it from the company, but the company wouldn’t sell because the other stockholders didn’t want that level of dilution.

In that case, the auditor took the position that it was compensatory. We mustered a variety of arguments and convinced them that, in that instance, it was not compensatory. Each individual situation is looked at on its own.

Are there other factors that would dictate whether something is considered compensation or just a stock sale?

One of the factors is: Who are the people selling the stock? Are they current employees or former employees or other investors or a whole wide group of people all at the same price? If you’re not just targeting employees, and instead including shareholders who don’t work at the company, then there’s a stronger argument that the intention is not compensatory and that everyone can treat the sale as capital gains.

Is it possible to structure these transactions in such a way that it’s not compensatory?

It depends on which existing investors participate. If it’s existing investors with a material stake in the company and a seat on the board, that can make things look compensatory.

We had a third-party tender happen earlier this year for a company where we were involved in the deal early. We told the company: Find buyers who are not related to the company. Then at the end of the day, a couple of the existing investors joined the buying syndicate. These were very small—less than 5% holders that weren’t on the board—and we looked at that and we determined it’s okay. But there’s no threshold enshrined in law. It’s all a judgment.

What are the negative consequences if an auditor, after the fact, comes in and says a tender offer was compensatory?

The secondary market has evolved so rapidly that it’s difficult to project out too far into the future. The trends we are seeing today point to massive geographic expansion in the market as private companies across the globe start to become more comfortable with raising private capital and delaying a public offering. This changing landscape has led to NPM completing transactions in 21 states, in addition to Canada, Europe, and South America, and doubling its transaction volume in the past two years. We anticipate that the global expansion of this market will continue to accelerate in the coming years.

Is there anything else companies should keep in mind as they begin to think about doing a tender offer?

There’s no cookie-cutter solution for an employee tender offer, owing greatly to the complexities of a single transaction. Each transaction has its own set of facts and circumstances, and each structure has to be thought about and tailored to take into account the nuances of the transaction. People have to think carefully about these issues because sometimes when you fix one problem, it creates another. You have to look at the total circumstances and figure out the best structure for a given fact pattern.

Related Blog Posts

https://www.founderscircle.com/wp-content/uploads/2024/04/All-Things-Equity-2.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-04-19 11:42:012024-04-19 11:42:014 Considerations To Craft Your Company’s Equity Strategy

https://www.founderscircle.com/wp-content/uploads/2024/04/All-Things-Equity-2.png

400

800

Matt McCue

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Matt McCue2024-04-19 11:42:012024-04-19 11:42:014 Considerations To Craft Your Company’s Equity Strategy https://www.founderscircle.com/wp-content/uploads/2023/10/Evolution-of-Exec-Comp-Blog-Featured-Image-555x528-1.png

528

555

Anil Sharma

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Anil Sharma2023-10-19 19:37:572023-10-19 19:37:57Evolving Your Compensation Plan on the Road to IPO

https://www.founderscircle.com/wp-content/uploads/2023/10/Evolution-of-Exec-Comp-Blog-Featured-Image-555x528-1.png

528

555

Anil Sharma

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Anil Sharma2023-10-19 19:37:572023-10-19 19:37:57Evolving Your Compensation Plan on the Road to IPO https://www.founderscircle.com/wp-content/uploads/2023/10/Navigating-Liquidity-Blog-Featured-Image-555x528-1.png

528

555

Anil Sharma

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Anil Sharma2023-10-11 17:29:302024-01-09 16:38:41Navigating Liquidity During Market Uncertainty

https://www.founderscircle.com/wp-content/uploads/2023/10/Navigating-Liquidity-Blog-Featured-Image-555x528-1.png

528

555

Anil Sharma

https://www.founderscircle.com/wp-content/uploads/2022/02/fc-logo-updated-600x189.png

Anil Sharma2023-10-11 17:29:302024-01-09 16:38:41Navigating Liquidity During Market Uncertainty